Some of the most recognizable trends shaping the future of the banking industry are applications, innovation, digital, digital, and more digital. However, another trend is becoming increasingly prominent: "net zero."

The history behind us has had several pivotal moments, and some that marked the beginning of industrial revolutions – the printing press, the power of water, steam power, mass production, assembly lines, electricity, computers, automation, and the internet. The COVID-19 pandemic has profoundly impacted humanity in all aspects, and banking as we knew it is on a path of transformation, turning it into an industry we did not realise just yesterday.

Some of the most recognizable trends shaping the future of the banking industry are applications, innovation, digital, digital, and more digital. Banks will be everywhere around us. However, another trend of banks' omnipresence is becoming increasingly prominent – the "green" trend: "net zero."

What is "net zero"? Simply put, the world aims to strike a balance between the emitted carbon dioxide and the amount removed from the atmosphere, meaning that the added gas is at the same or lower level than what is used up.

To reach this point, everyone – from countries and companies to individuals – must combat climate change, and it must be their top agenda. There is no room for excuses for anyone to claim that it does not concern them. This applies to banks as well.

Investors and regulatory bodies will not be satisfied with empty environmental promises in the future, as they call on banks to become more significant players in defending the planet and achieving "net zero" status. We expect that there will be regulatory measures defining independent audits to confirm that banks are acting in line with their public statements on environmental standards, and, more importantly, banks will face immense pressure to redirect their financing, and therefore earnings, from companies characterized as polluters worsening the greenhouse effect to those dedicated to sustainable energy. This will be the most significant test for banks, considering that oil, gas, and other fossil fuel companies provide them with stable and predictable income.

The Environmental and Social Management System (ESMS) was introduced previously. The International Finance Corporation (IFC), a part of the World Bank Group, published a handbook for its implementation as far back as 2015. Companies face numerous significant environmental and social challenges, and none of these challenges is insurmountable. However, they are not managed effectively or adequately assessed. In that case, they can cause not only harm to a company's profitability, damage its reputation, and hinder future business development.

Implementing an Environmental and Social Management System (ESMS) can have direct business benefits. Energy and material use reductions can impact lowering operational costs. Reducing waste generation and disposal and recycling can minimize waste disposal costs, which rise over time. Specific organic waste can be converted into fuel or energy, enhancing sustainability and saving on operating expenses. An ESMS can help you build processes to reduce costs compared to industry standards and identify potential savings in production and operational expenses. The role of banks here is twofold. As significant economic entities in any economy, banks must ensure that they do not invest in commodities that do not contribute to environmental protection and social management to preserve their future profitability, reputation, and prospects for future business. Like any other economic entity, they contribute to the common good in their business operations.

What are the most significant "cleantech" trends in 2022 destined to reduce carbon dioxide emissions and tackle climate change significantly, and what should banks have in their portfolio?

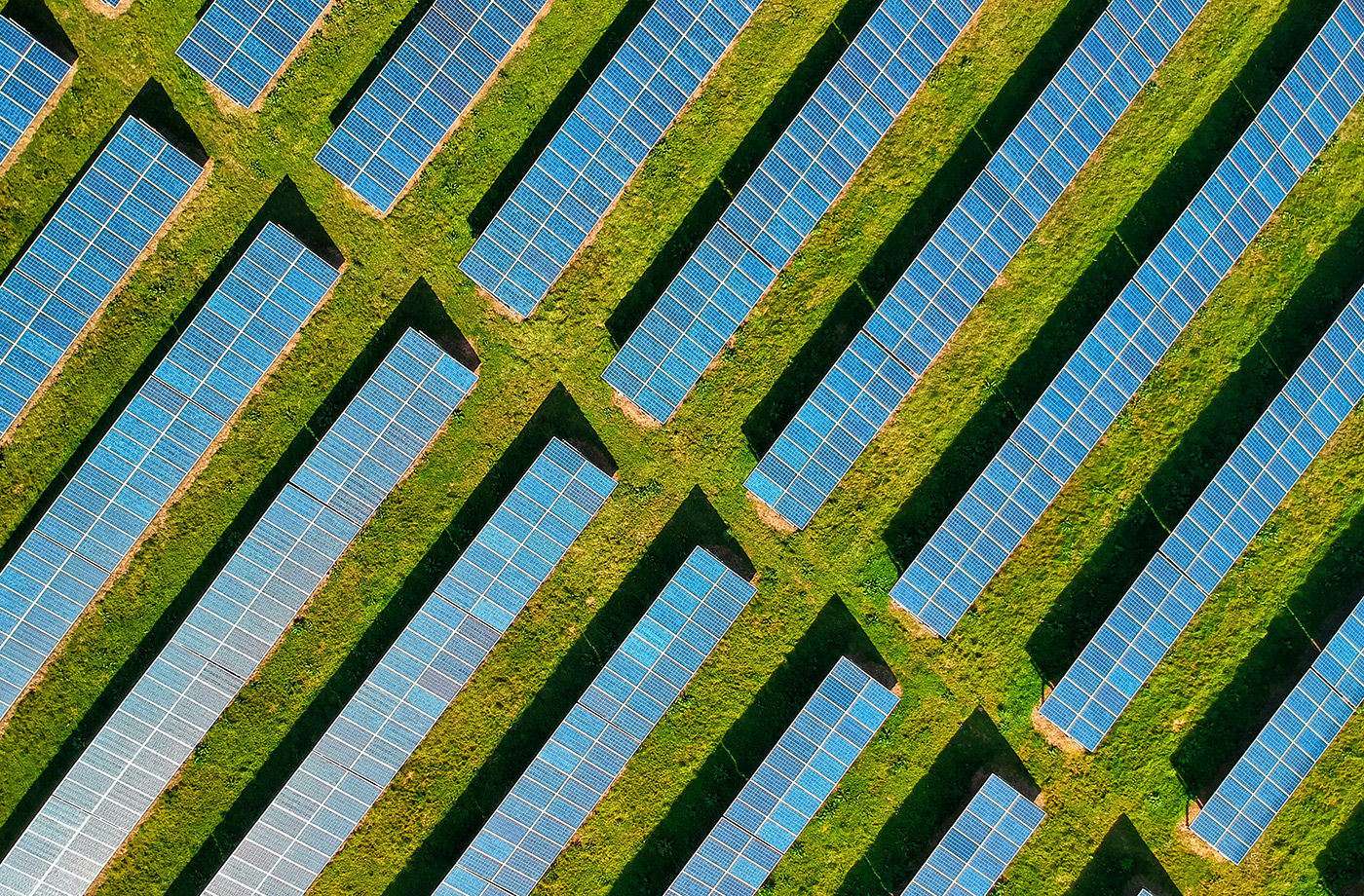

Although renewable energy sources are one of the cheapest generators in most world markets, due to supply chain issues increasing solar module and steel prices, there has been an unexpected increase in total investment, resulting in a stagnation in the decline of cost per installed watt. However, it's essential to consider the overall system value. Bank consolidation around renewable energy sources, coupled with significant green financing incentives, has reduced capital costs for renewable energy sources. An increase in solar farms with an output of less than 5 MW globally is expected to be over 20% in 2022. One way to ensure that this growth continues unhindered, that global supply chain and flow issues are overcome, and that the investment per installed watt continues to decline is to move the production of infrastructure elements for renewable energy sources as close as possible to the installation sites.

Wind turbine manufacturers have continued to invest in further development. Wind technology is shifting towards innovations in more giant turbines and the use of recycled materials. Wind turbines have increased their capacity by 50% in just three years. With further research into material combinations, waste reduction, and increased recycling, Siemens Gamesa produced its first recycled blade in 2021. Further wind turbine development is focused on floating wind farms, which may be geographically out of reach for some. Still, large projects in this segment are expected to be announced in France and the United Kingdom this year. Currently, the largest project initiated in 2021 is the 50 MW Kincardine project on the shores of Scotland. This year, a record is expected to be set in Norwegian waters: Equinor's 88 MW Hywind Tampen, which will supply the company's oil and gas platforms.

Lithium-ion battery prices increased by 10-20% towards the end of 2021 due to rising raw material prices, increased demand in the auto industry, reduced purchasing power of energy storage system integrators, and the geographic concentration of LFP in China. However, despite all of this, the cost of energy storage in batteries remains competitive compared to alternative technologies, although further price reductions are not expected until 2024.

Corporations and small to medium-sized enterprises will use renewable energy sources for various reasons. Some do it primarily for regulatory reasons to reduce fines and penalties for potentially increased carbon dioxide emissions. Others want to lower electricity costs, while some aim to reduce the risk of power supply disruptions.

More precise regulatory frameworks have paved the way for the development of green hydrogen, with 15 GW of electrolysis capacity worldwide in 2019, 70 GW in 2020, and up to 250 GW in 2021.

Two thousand twenty-two new regulatory incentives for carbon capture and storage (CCUS) industry development are expected worldwide. In 2021, this industry grew by 26%. Regional diversification is likely to continue in 2022, although North America and Europe dominate these markets.

As you can see, there is significant potential, and banks are one of the driving forces that will contribute to green development by shifting their investments from fossil fuels to the low-carbon economy and low-carbon and climate-resilient (LCR) infrastructure. In Serbia, over 70% of electricity is generated from coal; per capita, we have Europe's highest coal-based electricity production. In Serbia, there are several projects for 5-10 MW solar farms, where the main stumbling block is financing, and these projects can be a good start in reducing our carbon footprint.

Some banks will embrace change and adopt a stricter stance on their clients' environmental footprint and operations. Some will only simulate green business. Some banks may be willing to sacrifice their short-term goals for long-term progress, which, if defined by regulation, will be the only way they can operate. But no matter what path leads to this, the green wheel has started turning, and green is becoming the most critical colour of money once again – because a bank must be healthy.

Serbian(Srpski)

Serbian(Srpski) English(Engleski)

English(Engleski)